[Note: this post has been updated for 2017 2018 2021 data. I plan to continue updating it every year or few.]

A long while back, a reader wrote:

“Hey, Nords, any chance you’ll do a summary post about your FIRE history? I’m really interested to hear how your net worth and income have gone up.”

Life is good: my spouse and I recently pulled off an epic seven-week “slow travel” Mainland trip on military flights. (I’ll post more about Space-A travel another time.) Now that we’re caught up on household chores, I’m ready to catch up on financial topics.

I’m surprised to realize that we now have 15 19 years of experience at being military retirees. (Where did the time go?!?) We spend most of our year at home (or at the beach) enjoying our Hawaii lifestyle. When we’re off the island, we prefer to spend weeks at a location with more time for strolling, thinking, discussing, and (in my case) writing. No worries: on this trip our entire Nords ohana got in lots of surfing too.

During our travel, I wondered whether I should even write this post. A few months back I asked the opinions of a bunch of other personal-finance bloggers who share their finances with their readers. I ruminated over the pros & cons of sharing more personal details. For example, I’ve been tracking our income since the 1970s(!) and I could publish frequent updates on Rockstar Finance’s net worth list along with hundreds of other bloggers.

Good reasons to share our numbers

I think our track record can inspire people who are striving for their own financial independence. We’ve been FI since 1999 and I retired from active duty in 2002. Our first decade of retirement slammed into not one but two of the nastier recessions of the last century. Yet today, our finances have bounced back to new highs and life is better than ever.

For starters, we’re living proof that the 4% Safe Withdrawal Rate works. It survives bear markets. The research has been validated by peer review and replication, yet the computer simulations have a number of gaps which will always worry people about its failure rates. (Pro tip: Humans are smart enough to use variable spending.) The biggest danger to a FI portfolio is “sequence of returns” risk: a recession at the beginning of a retirement could wipe out so much of the portfolio’s value that it can’t recover from its first decade of withdrawals. This issue is easily avoided (Hint: buy an annuity or start with an asset allocation of two years’ expenses in cash) yet everyone worries. You’d hate to walk face-first into the World’s Worst Recession and get shoved right back into the workforce.

Our investments survived recessions not just once, but twice. The 4% SWR math worked great, although we investors were freaking out a little.

We could share our financial numbers to help inspire other military families. Behavioral financial psychology is always more powerful than math or logic, and it helps to know that other people have been through it too. Whenever your FI math displays a 95% success rate to your highly logical cerebral cortex, then just behind that forebrain your emotional amygdala is whining about a 5% failure rate and hijacking all of your self-confidence. Even worse, when you try to explain the logic of the 4% SWR to your family & friends you’ll encounter a bunch of “But what if… ?!?” questions which could scare even Warren Buffett. It’s no surprise that many people reach their FI numbers yet keep on working for “Just One More Year” Syndrome.

S&P500 index history 2000-2017.

Well, my spouse and I felt our amygdalas twitch a few times, especially in October 2002 and March 2009. Maybe we can help reassure people by sharing our numbers.

Reasons to not share our numbers

Once I hit “Publish!” on our net-worth numbers I can’t just erase it, and I don’t want to screw this up. I want to help people without irrevocably crossing a #humblebrag line.

Ms. Our Next Life put my concerns very succinctly: “Comparison is the thief of joy.”

We already know that it’s a bad idea to keep up with the Joneses. Yet if we post our net worth then we’re tempting you to keep up with the Nordses. Humans all have different costs of living (and different spending choices), yet we’re competitive animals. (We even try to out-frugal each other on Internet forums.) I’m trying to NOT be so competitive. I just want to reassure military families that financial independence is within your reach, and I don’t want our numbers to discourage anyone.

Comparison might make you feel pretty good if your net worth number is longer bigger than mine, but what if you’re just starting your FI journey? It’s hard enough to track your spending and cut out the waste and maximize your Thrift Savings Plan contributions for a goal that you believe in. When you see the results of someone else’s trek– 15 years after they cross the finish line and maybe 30+ years ahead of you– it’s very difficult to believe that your numbers could grow so big. Our success might be more discouraging than inspiring, despite all of the mistakes we made along the way.

Our numbers aren’t relevant to yours. You just want to know that you can go from “enough for the 4% SWR” to “more than enough for the rest of your lives” without having to worry about portfolio failure.

Nobody mentions those failures

Everyone talks about the failure rate of the 4% SWR, but have you ever met someone who’s been forced back into the workforce because of it?

I know a few people. They had their numbers, but one couple freaked out over stock-market volatility. Another person was bored and unfulfilled by all of their free time. (FI means that you have to be responsible for your own entertainment.) Another reached FI on a very undiversifed asset allocation plan which failed after their favorite stock’s first dividend cut of the Great Recession. They went back into the workforce, worked out a diversified asset allocation, and achieved FI again a few years later.

We don’t hear about those failures. Nobody wants to talk about them.

Instead, we focus on the winners. It’s easy to watch the credits roll at the end of a movie and say “Yeah, that was a good flick.” You liked it because everybody loves a winner. But when you reach FI and declare your freedom, you’re still in the first act of your FI movie. How will the next couple of acts turn out? Will it be a heroic saga or a tragedy?

Let me set the stage for the potential failure of our financial independence, back when we didn’t know how the movie would turn out.

In late 1999 we crunched the numbers and realized that our portfolio was big enough for the 4% SWR. We wouldn’t even need a military pension. We could spend the rest of our lives from our investment portfolio.

If you’re familiar with the 1990s Internet stock-market bubble, you can imagine that a lot of people had our epiphany. No worries, it was the “new normal”. This time everything was different, and this time we really meant it.

Barely two years later, as I was signing my active-duty retirement worksheet, the situation was a quite a bit different.

Life still happens to you during financial independence

Let’s break down the bullet points:

- We knew that my pension would cover our mortgage, but what about hyperinflation during a recession?

- My spouse left active duty for the Reserves. Her pension would be delayed for 20 years… if she even qualified for one.

- The stock markets were closed after the 9/11 attack, then lost over 10% in one day.

- Never mind retirement. Would my spouse and I mobilize for the war?!?

- The price of college was rising faster than our nine-year-old daughter’s college fund.

- Hawaii was in a decade-long real-estate recession, and our rental property was worth less than we’d paid for it.

- We had no cash flow from our rental property… and no rent increases, either.

In 1999 we were FI on just our investments. Two years later, however, the value of that portfolio was melting down faster than an ice cube on a Hawaii beach. Nobody knew how long the bear market would last.

S&P500 index value during September 2001.

At least I’d been approved for my military retirement. My pension covered a little of the spending and we still had (barely) enough portfolio value to make the math work for our expenses. The 4% SWR is never pretty during a recession, but it would work during this one.

The good news? We had the basics covered and I could always get a job through my submarine veterans network. (Hey, back then Linkedin was just this goofy startup going up against the Monster juggernaut.) I could run a power plant or teach a class.

I retired in June 2002 and the stock market kept dropping. Not what we had in mind. Let’s just say that in October 2002 the Nords household had a tense financial discussion… and we decided to stay the course. It’s a really good thing that the markets bottomed out that month, because my cerebral cortex was running out of cheery optimism about the statistical success rate of the 4% SWR.

With that experience behind us, you can predict that Act II of our FI movie would be more cheerful, right? Um, not quite.

I’ll spare you the gory bullet points on the Great Recession, but I’ll mention that our investment portfolio dropped 58% from the 2007 peak to the 2009 trough. We were cool with the first 25%, but the rest was ugly. We endured over 600 days of pain in the assets, made even worse when it was punctuated by multiple head fakes from the stock market. By 2009 nobody believed anymore that we’d really reached the bottom.

S&P500 index value 2007-09.

During the next three years of the recovery, most investors were still waiting for the economy to pitch over again and dive for an even deeper bottom. There was plenty of gloomy data to support the markets losing 90%, just like they did during the 1930s.

Believe it or not, we stayed the course during the whole thing. I re-read my favorite investing books (“financial comfort food”) and we all vented our concerns on Internet forums. Our family focused on getting our daughter ready for college and we did a lot of surfing. Ironically I was finishing the draft of a book about military financial independence, and I worried that I’d have to rewrite its ending.

Have I beaten this point into the ground yet?

Emotions can derail the best of FI plans, even when the 4% SWR is working.

Let me finish on a cheery note. Act III of our financial independence puts this investment angst in perspective.

In 2015 I had an emergency appendectomy. I went from “Ow!” to the OR in less than 24 hours, and the surgeon still worried that I’d waited too long. Everything came out all right (so to speak), but as the morphine kicked in I had a much different epiphany than 1999. While the medical staff cleared a table for one and my spouse tried to keep a smile on her face, I reflected that those years of financial independence had been the best of my life. I was very happy that I hadn’t spent them working for a paycheck, let alone doing submarine patrols.

Yeah, I’d never had morphine before. It was a big dose. Wow.

Today I know that it’s much better to worry about your portfolio survival than to worry about your own survival.

Better yet, it looks like we’re finished worrying about our portfolio survival.

Now for the numbers.

The net worth numbers… in percentages.

After weighing the feedback of my financial blogger friends, I hedged and decided to put our numbers out there in percentages.

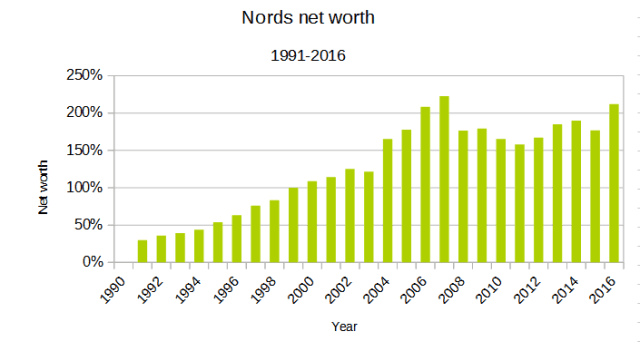

Here’s the excerpt from our net worth spreadsheet. Its cells cover from 1977 to 2016 (yes, I’m a Navy nuke and a money nerd), but for clarity I’ve focused on the relevant years. I set 1999 as 100% and indexed all the other numbers to that FI starting point.

Ironically, we didn’t start tracking our net worth until 1993 when we read “Your Money Or Your Life”. (Hunh– 22 years before my appendectomy.) I’ve logged 40 years of income and 30 years of spending data, but we only reconstructed our net worth back to 1991.

The graph tracks the typical exponential compound-growth curve up to 1999, and while we were building it I can assure you that curve seemed awfully flat for a very long time before 1991. (Humans suck at perceiving exponential growth, and the early years of saving for FI can be discouraging.) 1999 was the first time we reached the 4% SWR tripwire.

After 1999 you can tell that the curve flattened out around 2001, but it made up for lost time in 2004-07. And how ’bout that drop in 2008? We cut back our spending a little in 2009 but after that, we could see the asset recovery. I didn’t even notice the 2015 air pocket until I was drafting this post, and 2017 could end on an even higher note than 2007.

As long as those percentages stay in triple digits, it doesn’t matter how high they go. Our annual spending has been flat for most of the last 15 years. Our daughter launched from the nest in 2014, and our spending could drop even further during the next decade.

Now that our assets are twice as big as the 4% SWR, our spending is effectively a 2% SWR. We’re spending less than the long-term dividend rate of the stock market, which means that we could hypothetically live off the S&P500’s dividends without touching the growth (let alone the principal).

The other good news is that we’re immune from the sequence-of-returns risk which can savage a portfolio during the first decade after FI. Beyond that, trying to predict the financial future is an exercise in frustration.

Maybe someday I’ll talk about the dollar figures with a few more beta-testers while we’re sitting on the beach after a surf session. (I’m lookin’ at you, dual-military retirees.) Maybe someday we’ll talk about the details at a financial conference, or if you’re thinking about angel investing. (Pro tip: limit alternative investing to no more than 10% of your assets.) But at this stage of our lives, I think you want reassurance without getting mired in the significant digits.

[Update: here’s the 2017-18 2017-2021 data at >300%.]

Your turn: what do you want to share about your numbers? If you’re already financially independent, how’s that workin’ for ya?

If you’re not FI (yet!), then what are you doing to get there and how much longer do you think it’ll take?

Related articles:

REVEALED: Our Asset Allocation During Financial Independence

How Should I Invest During Retirement?

How Much Cash In A Retirement Portfolio?

How Do You Survive A Stock Market Crash?

Hey Nords! ;)

I have not, as of yet, come across a PF blog of people who have achieved FIRE without having the significant other on board. I could be FIREd if WE could keep our expenses down a bit more but…

“A happy wife is a happy life.”

WE’re getting better though.

Glad you finally revealed your numbers albeit incognito! Seriously, you brought up some good points about what can happen if you reach FI and then the markets collapse! I’ve been thinking about this a lot lately and just decided that my “retirement” will be from a job that I have to work, not from a job that I want to work. We’ve had a great bull run and I’ve already got my heart set on the next bull run. The only problem is no one knows when that will be or how long it will be.

Thanks Darren!

I think you’re right about having spouses on board. That’s not a financial problem– it’s a communication problem or even a marital problem.

Your spouse could be showing you exactly where the line needs to be drawn between frugality and deprivation. Frugality is challenging & fulfilling while deprivation is not sustainable. You might have been FIREd sooner but you probably would’ve been unhappy. Especially, as you’ve noted, if your spouse is unhappy.

No need to fear the next recession when you’re improving on the 4% SWR with the techniques of a two-year cash stash and variable spending. (4% SWR computer models are still struggling with that simulation code, but it’s working just fine for the humans.) And I like your idea of being FI from having to work, not necessarily from wanting to work. That makes a great 140-character meme!

We are dual Navy retirees. I have had no luck finding other duals to compare anything with. It would be nice to know how other dual military with no children have fared in their retirement years. DH retired 11 years ago at 40 and I retired 7 years ago at 43. We have been using our GI Bill for school for the last few years.

My wife and I are dual military retirees (Army). I retired 4 years ago and my wife retired just a couple of years ago. We initially planned to retire on the same year (we hit 20 years with 2 weeks of each other) but staggering our retirements worked out better for us. Kids are all grown and have flown the coop, with the youngest a USAFA grad but now a CPT in company command in the Army. She is keeping the “family business” going…and, I like to say, business is “booming” (pun intended).

The wife and I are FI and RE…thanks in no small part to Nords giving us the confidence and reassurance after looking at our numbers and reading about his own story in this blog.

Thanks, Mel!

KLG, there’s not enough dual-military retirees to populate a database for a statistical analysis, but… all of the dozen-plus dual-military retiree couples who I personally know have assets ranging from “more than enough” to “way more than enough”.

The real power behind the military pension is not the amount of money. It’s the cost-of-living adjustment and the cheap healthcare.

Good again to hear from you Nords. My fear was that you joined one of those hippy free love communes on the Big Island. As to the economics of your personal case study three key points as always. -you kept totally invested relative to your risk tolerances over the various markets ups and downs. -You did not allow emotions or urges or fear dictate your investment decisions. -You kept spending or outflow relatively even during the periods cited.

All deal not so much in strict dollars and cents but in the area of behavioral economics and why people behave the way they do with money. Or what money means to them. FI is just as much a mind-set and emotional/psychological space as it is an amount or size of one’s accounts. And as you have said many times, FI is not a magic number but freedom to do what one wishes, when one wishes. Which was very common in the era of the old cliff vesting model of military retirement, well see in the out decades how the BRS provides. My fear for many, not all that much to be honest.

Thanks, Peter, I’m open-minded about the commune but I’m not sure whether my spouse is interested…

I haven’t stopped writing but most of my output was going toward book manuscripts and reader questions.

Those three key points are straightforward in principle & logic, yet the emotions are a tad more difficult.

BRS is strongly focused on giving more assets to the 85% who don’t make it to a military retirement. Among those who beat the 1-out-of-6 odds and retire, I suspect it’s revenue-neutral for most. It’s more profitable for those who aggressively invest their matching DoD contributions, and it’s almost certainly more profitable for those who have a large continuation pay multiple in their specialty..

We are doing well after FI. I’m mostly retired and the missus is looking to join me soon.

Your net worth graph is great. I do have one question.

How come the net worth is just now reaching the 2007 level? From what I gathered, you didn’t withdraw much during this period. from 2007 to 2016.

Our net worth increased dramatically during the last decade. That’s because we still have income and we kept investing.

Once we both stop working, we won’t be able to add much new money.

Thanks, Joe, good to hear from you!

I didn’t go into detail on our spending, other than “flat for most of the last 15 years”. The drop in 2010-11 was discretionary from three factors: a home renovation, a number of charitable donations, and a couple of investments in startups (which flamed out).

I think 2006-07 were outlandishly bullish years, too, and our investment portfolio was ballooning in value. I spent a good bit of time in 2007 slowly liquidating my individual investments in large-cap stocks. Valuations had gone from “high” to “ridiculously overpriced”.

If our net worth vaporized from 212% back down to 100%, we’d still be FI. I wouldn’t be sponsoring the bar tab for FinCon but our lifestyle would not change. As of today, though, the 2017 number is higher than 2016 by about seven percentage points. I hope that’s not a harbinger of the next recession, but it wouldn’t affect our lifestyle.

You picked a very good decade for continued investing! We have no plans to add to our portfolio.

Your statement “Humans suck at perceiving exponential growth” really resonates with me. I think one reason younger people (my previous self included) make poor financial decisions is they can’t foresee the exponential long term effects. A new car purchased right out of college… It would be great if there was some way the message of compound interest could be made in a more concrete way to people just starting out.

Thanks, MrInTheWheat, at this point I’m barely attracting any attention on the issue.

I’d love to know a better way to show people how compound interest works for them!

In this article you reference a 4% withdrawal rate but then also state that your spending has remained relatively flat. Am I to understand that you withdrew from your portfolio at an (initial) 4% rate and maintained a fixed withdrawal amount (same amount as the 4% equaled the first year) or that you withdrew 4% initially and then increased subsequent withdrawals by the rate of inflation?

Good point, Phil, we started with the 4% Safe Withdrawal Rate (initial 4% and then raising withdrawals by the rate of inflation). The excess (over our usual spending) went to charity.

The portfolio still grew quickly (as the 4% SWR statistics show is the usual result) despite two recessions.

If you start your financial independence with a fixed 4% withdrawal rate then you’ll do even better than the 4% SWR. You’ll automatically withdraw fewer dollars during recessions (because your portfolio shrinks during the market’s down years).

One key point about the 4% SWR is that, despite two nasty recessions, our portfolio still grew faster than our inflation-adjusted spending. When that growth happens, your withdrawal rate sinks below 3% (even if you robotically follow the 4% SWR method.) After 5-10 years your portfolio becomes immune to the sequence-of-returns risk.

Another key point is that people should stop worrying about the failure rate of the 4% SWR and instead use it as a tripwire to launch their FI. The best insurance against portfolio failure is some annuitized income, and for most people Social Security is more than enough. (A military pension is also quite sufficient.) People can use variable spending schemes to get through a recession, or keep two years’ expenses in cash for the first decade of FI, or even earn a little part-time income.

Most importantly of all, people should not prolong their working days out of “Just One More Year” syndrome. Too many of my friends have died at work because they were afraid to live off the 4% SWR.

Thank you so much for taking the time to explain this to me. I’m grateful for the information you provide here and your willingness to assist others who cant as easily grasp this stuff.

So if my understanding is correct:

A 4% initial withdrawal rate, increased yearly at the rate of inflation, is pretty safe.

A 4% withdrawal rate based on the value of the portfolio each year is even safer.

A 4% initial withdrawal rate that never increases or decreases (withdrawing the same amount as the 4% equaled the first year) year after year should be the safest.

Does this sound correct?

Phil, you’re missing the point but I’ll answer your questions first.

The 4% Safe Withdrawal rate (your first line) is indeed pretty safe because humans are not robots. You don’t have to cut spending during a recession, but people will do it anyway.

The “4% withdrawal every year” is safer because it always leaves you with 96% of your portfolio. You’ll never run out, even if you only have 25 cents left. However in volatile bull/bear markets you’ll withdraw way more than you need, or way less than you want. People generally prefer a more predictable withdrawal.

The “4% fixed” is indeed the safest because your portfolio probably rises over the years with inflation (especially if your asset allocation is heavily invested in stocks). It turns out that most financial advisors have noted that most of their clients actually have declining spending during retirement until just before the end of their lives. Search for the term “retirement spending smile” for more info.

Here’s where you’re missing the point: you’re trying to make these withdrawal systems absolutely safe, and that’s going to keep you in the workforce for far longer than necessary. You can guarantee the survival of a portfolio with an annuity (as much as there are guarantees for portfolio survivability), and for most retirees their Social Security is sufficient annuitized income.

Instead of trying to make the 4% SWR even safer, use it as a tripwire. When you reach the point that your assets are 25x expenses, then you’re almost certainly financially independent. You’ll review your spending every year for the first decade or so, and you’ll lower your spending during bear markets (because you’re a human). Maybe you’ll keep a year or two of expenses in cash for bear markets for the first few years of FI (because of sequence-of-returns risk). You might discover a hobby which pays for itself or even generates a little side-hustle income.

While you’re doing all of that, your FI portfolio will be chugging along making you richer in over 80% of the historical simulations. If you happen to encounter a 16-year bear market like 1966-82, you’ll have an annuity (like Social Security). You might even return to work for 10 hours a week to get your finances over a bad recession (or for a fantasy vacation). Most people don’t want those jobs (even in a recession) because they can’t support their living expenses. But you’ve already covered your living expenses (with your FI portfolio) and you’re just trying to give it more breathing room.

Doug, I’m grateful for you sharing your journey, & especially your response to Phil in these lines:

“Another key point is that people should stop worrying about the failure rate of the 4% SWR and instead use it as a tripwire to launch their FI. The best insurance against portfolio failure is some annuitized income, and for most people Social Security is more than enough. (A military pension is also quite sufficient.) People can use variable spending schemes to get through a recession, or keep two years’ expenses in cash for the first decade of FI, or even earn a little part-time income.

Most importantly of all, people should not prolong their working days out of “Just One More Year” syndrome. Too many of my friends have died at work because they were afraid to live off the 4% SWR.”

Your discussion of the failures names the unknowns & your prompting to trust the process is the final clarity we needed. After reading this article today (much after it was written), we are fully launching our FI life. Appreciate your advice, from a “bubble head” to another :)

Outstanding, Tom, and enjoy the ride!

Good info on the percentages of your net worth. Basically, you are 2x as rich as you were, and that’s with taking money out and everyone living in fear.

Thanks, LT! Yep, the numbers are showing that the 4% Safe Withdrawal Rate is working the way it’s supposed to work, and that the numbers are following the “high success rate” probability.

If there was going to be a failure of this portfolio, it would’ve happened during the first decade. Instead it’s growing faster than inflation, and at the long-term rates. Now that the SWR has dropped below 3%, it’s indefinitely sustainable.