Disclosure: This article is part of the Life Uninterrupted campaign sponsored by USAA. The #LifeUninterrupted campaign is designed to help future retirees learn how they can transition into retirement without worrying about financial interruptions. You can receive a free, no-obligation retirement review today by calling USAA.

Note: We are receiving a fee for posting; however, the opinions expressed in this post are my own. I do not earn a commission or percentage of sales.

After over 16 years of retirement, we’ve verified that we’re not spending fast enough. We have enough assets and income for the life we want, and for the rest of our lives. According to the statistics of the 4% Safe Withdrawal Rate studies, you’re likely to share the same experience. This post will help you figure out your retirement “Life Uninterrupted.” In other words, I’ll walk you through our 20 years of financial independence, how our spending had changed through the years, and how our retirement has remained on track the entire time – without financial interruptions.

If you would like a free retirement review from USAA to see how well you are on track, you can visit their site and schedule a free review.

In an earlier post, I promised more details on how our family financial independence life will keep getting better in 2019, and we’ll start by digging into our FI spending trends.

We have 40 years of spending history, so I think we can draw reasonable conclusions. I hope to collect at least another 40 years of data.

Track Your Spending and Cut the Waste

We'd decided to stick around for another tour.")

Starting the FI journey in 1987 fashions. Don’t judge.

I started budgeting in college when I finally got tired of running out of money. (“And this time I really mean it!”) A few years later when my spouse and I married, she elevated our skills to an Olympic level. I focused on the details by closely tracking our spending. Today our Quicken database has nearly 27 years of data in over 150,000 transactions.

While I dig into the numbers, my spouse is the big thinker in our couple. She usually pulls us back from my microscope to ask thoughtful questions.

Once we had a good track on our expenses, it was easy to find the waste. After a few thoughtful discussions, we were routinely aligning our spending with our values. (Pro tip: each of us has a monthly personal allowance for guilt-free spending with no judging.) Our savings rate shot up and we were on the road to financial independence.

Our “Why?” of FI was to regain control over our time (and our lives). We didn’t know how long we wanted to stay on active duty, and we were taking it one obligation at a time.

Today that’s still our “Why?” We don’t know how much time (or lives) we have left, and we want to make the best of both.

Financially Independent: Now What?

Starting our FI life.

By late 1999 we’d saved and grown our investments to reach the tripwire of the 4% Safe Withdrawal Rate. (Hey, it was the peak of the Internet bull market. Millions of people reached FI that year.) It was also the first time in my military career when I was confident of earning a military pension. (That was not at all assured during the 1990s drawdown, because I’d fallen off the career track and then failed to promote.) Since I had less than three years to go in a billet which did not suck, I decided to hang on for the pension.

Financial independence paid another unexpected dividend: my spouse decided to leave active duty for the Reserves. Her last active-duty paycheck was in early 2001 and I retired in mid-2002.

It was an “interesting” time to stop working: the Internet recession was in full roar, and (in retrospect) the markets bottomed in October 2002. By that point, of course, everyone was convinced that the stock market and the economy were both going to zero.

We had done our reading and our analysis, and we were pretty sure we had enough investments for the lives we wanted. We started withdrawing money at the 4% Safe Withdrawal Rate.

Are you on track for financial independence? Get a free retirement review from USAA. You do not need to be a USAA member to take part in this offer.

16+ Years of FI Spending

2003 was our first full year of FI spending.

Before then, we did what every newly-FI person does: we reviewed every penny of our assumptions to make sure we’d caught all of our mistakes and still had a sustainable plan.

We rebuilt our budgets from zero. We reviewed every monthly bill, and we made a lot of phone calls to ask for our “retiree discount.” We had more time to find online bargains and shop at garage sales. We also kicked our do-it-yourself skills into high gear: more home-cooked meals and more home maintenance & repairs. We did our own chores and yardwork (and got plenty of exercise). We drove our (used) cars a lot less, but we still drove them into the ground.

Joining the family business.

Yet we maintained the parts of our lifestyle that we’d worked for. We ate out whenever we wanted, and we still enjoyed plenty of travel and other entertainment.

Life went on, and it was very good. We navigated our daughter’s teen years and she started her own path to FI. We endured the Great Recession, although our investment portfolio briefly dropped over 50% from peak to trough. We explored new interests. (Surfing and taekwondo.) Since I’m an engineering nerd, we built our own photovoltaic array and our own solar water-heating system. We survived our 40s, and now we’re in our… high… 50s.

I tracked every penny of our FI spending in Quicken up through 2015. In 2016, I delegated that task to Personal Capital (we only use Personal Capital to track investments and spending, we do not use their investing service). We spend very little in actual cash, so we still have a close track on our spending.

During our first decade of retirement, we knew that a bad bear market could derail our 4% SWR and kill our investment portfolio. We had contingency plans for the worst-case scenarios, but we never needed them. Now after 16 years, it’s clear that we are no longer vulnerable to the dreaded sequence-of-returns risk.

The Retirement Spending Smile

Click the image for a bigger version.

Michael Kitces was one of the earlier researchers to popularize what financial planners had observed for years: retirees start their spending at a sustainable rate, but then it declines.

A couple of years later, Wade Pfau’s analysis verified the conclusions about retiree spending. Researchers have shown that retirees start with a go-go lifestyle, later ease back to a slow-go phase, and eventually settle into a no-go routine. The majority of end-of-life spending (the other side of the smile) is for medical care.

We’ve been a very active family for our first 16 years of retirement, and we’re doing everything we’ve wanted to do. More importantly, we’ve continued our laser-like focus on cutting the waste. Today our bare-bones living expenses are the lowest we’ve ever had. We could live extremely frugally if necessary, but otherwise, we have more money for more lifestyle!

Last year we finally finished 16 years of Roth IRA conversions to pay lower income taxes and avoid mandatory distributions. Thanks to the analysis of Personal Capital, this year we’re moving our investments from expensive sector exchange-traded funds (with expense ratios of 0.25%-0.39%) to a total stock market ETF (0.04%), which will save us thousands of dollars a year.

One of our 12-year-old cars started racking up the repair bills, so we upgraded to a used Nissan Leaf– which recharges its battery from our solar array and will cut our gas bill by $400/year.

At the same time, we’ve optimized our entertainment spending. I’ve joked about “Travel while you can,” but we’re going to keep going as long as we can.

Retirement travel is actually cheaper than work vacations. We roam for months instead of weeks, living like locals and avoiding the tourist crowds. Travel hacking (airline miles and Space A military flights) has reduced our airfare while AirBnB and VRBO let us rent cheap apartments (with kitchens) for months. (We were travel hacking before it was cool.) We’re paying off-peak long-term prices instead of living like two-week millionaires at a resort hotel.

Our saving & investing has paid off. How has all of our optimization affected our retirement spending? I’ve spent about 10 man-hours crunching the long-term numbers, and I was surprised to see the big picture.

“Let’s Look at the Graphs.”

[Note: “Comparison is the thief of joy.” I’ve indexed our actual spending to a starting value of $100, and we show actual spending as a percentage of the value of our investment portfolio. Instead of being distracted by how much we spent or our place in our journey, you can compare these ratios to your own numbers and your own progress.]

In these graphs, our expenses are compared to only our investment portfolio. That’s all we were able to rely on when we reached FI, and it’s turned out to be more than enough. We weren’t counting on home equity in 1999 because the Hawaii real estate market had declined nearly 50% from its 1990 peak. My military pension came three years after 1999, and our rental’s cash flow began much much later in 2008.

In 2019 this all seems pretty straightforward in hindsight. 20 years ago? Not so much.

We did not have any crystal balls in 1999, and we certainly didn’t have any in 2001 when my spouse decided to leave active duty. We made those decisions for a better quality of life because we had enough investments for the 4% SWR.

The 4% SWR’s 80% probability of success came through.

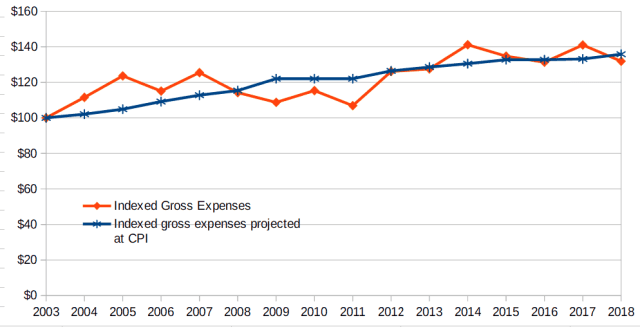

The first graph shows 16 years of retirement spending. The orange line is indexed to a starting value of $100 and has risen over the years to $132. The blue line starts at the same origin but assumes that our spending grows at the 4% SWR’s rate of inflation. After 16 retirement years of the Consumer Price Index (the same inflation index as the military pension and Social Security), our spending should be at $136.

We wandered above and below that 4% SWR curve, yet we still ended up on the low side.

Orange (actual) is pretty close to blue (the CPI trend).

In 2004-05 we were spending on home improvement projects like our photovoltaic array and our solar water heater. We were also ramping up our taekwondo training and doing more travel during school holidays.

We spent 2008-2011 coping with the Great Recession. Humans are not 4% SWR robots, and we traveled to less-expensive locations because we felt uncomfortable about partying like it was 1999. By 2011, though, our daughter had started college. We ramped up our lifestyle with home improvement and even more travel.

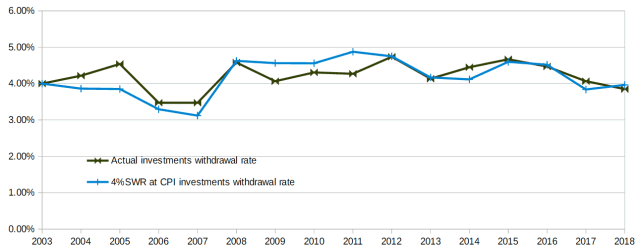

How did that affect our withdrawal rate?

Again, this graph indexes our first full year of retirement to the 4% SWR. The black line shows our actual spending divided by our investment portfolio’s value. In 2006-07 our withdrawal rate dropped below 4% because the value of our investments grew much faster than our spending. That went the opposite direction in 2008-12 as our investments took much more of a beating than our spending.

The blue line shows what our withdrawal rate would have been if we rigidly spent the 4% Safe Withdrawal Rate by starting at a 4% withdrawal and raising our spending by the rate of inflation. The graph’s variation is caused by the changing value of our investment portfolio, yet everything recovered and converged back to that 4% line by 2017. Now it’s trending down below 4%.

We’ve been withdrawing from that investment portfolio for over 16 years and two very scary recessions. Despite the volatility, it’s doing just fine. We know our expenses will be lower in 2019, leaving more in our investments to grow even faster.

The Go-Go Years

We’re having as much retirement fun as our bodies can handle. (I don’t surf 20-foot waves anymore, but 10-15 feet is still fun.) Our retirement spending is in the middle of Michael Kitces’ “go-go” years of the retirement spending smile. We’ve kept it up for over 16 years and our investments have done just fine.

Although our total spending has tracked the 4% SWR, our non-discretionary spending has dropped dramatically since 2003. We have lower utility bills, lower insurance expenses, lower vehicle expenses, a lower interest rate on our mortgage, lower expense ratios on our investments, and a much lower income-tax bill. We’ve raised our family and our daughter is off our payroll. We’re eating healthier while spending less. Even home maintenance (and improvement) is cheaper.

I haven’t had a haircut since early 2002. We’re really racking up the savings on that one.

Controlling the essential expenses has given us a lot more to spend on entertainment.

Yet even our entertainment is less expensive. I’ve bought all the surfboards I can handle. (Surf wax is cheap.) Empty-nester travel during shoulder seasons costs less than family summer vacations. Travel hacking has dramatically improved, and these days we enjoy the occasional first-class lie-flat seat. (A sleeping bag and a yoga mat on the deck of a military cargo jet is still the ultimate aircraft lie-flat experience.) We can see plenty of room to ramp up that lifestyle.

More importantly, my inflation-fighting military pension now protects us from volatility risk and sequence-of-returns risk. The CPI has gone up a total of nearly 40% since we retired, but our annuity income has also risen by nearly 40%.

The Slow-Go Years

Doonesbury’s “Ol’ Surfer Dude” rocks.

We’ve already verified that our current lifestyle expenses are sustainable, and I’d like to think that I have another 30 years of travel and surfing in me. I’ll let you know how that goes.

In the meantime, we’ve won the financial independence game. The major risks have already been covered, and now we’re just running up the score.

Social Security is on the horizon if we need it. (We won’t need it.) We can finally afford the opportunity cost of our rental property. My spouse’s Reserve pension starts in 2022. Philanthropy and estate planning are in progress.

Our No-Go Years

I don’t have a clue on that part of our lives, except to hold it off as long as possible. There are a few surfers in our lineup who are in their 80s. I know of a couple of famous surfers who were paddling out in their 90s. I may not be popping up on a longboard, but if I can’t paddle a stand-up board then I’ll still be out there in a kayak.

When my father passed away in 2017, he passed on an inheritance (and some life insurance) to my brother and me. We’ve invested that in a total stock market index fund to self-insure our long-term care expenses. We expect at least 20 years of growth out of that fund before we’ll even think of using it.

USAA’s “Life Uninterrupted” Campaign – Get a Free Retirement Review

As I was researching and writing this post, I’ve realized that we’re years ahead of USAA’s new “Life Uninterrupted” campaign.

We saved for retirement as aggressively as we could, but we were keenly aware of the line between frugality and deprivation. (The former is challenging & fulfilling and you feel like you’re winning, while the latter is painful and unsustainable.) When we declared our financial independence, it was at our desired lifestyle with much more than a bare-bones survival budget.

It’s also a highly individual choice! These days the FI community is exploring categories like FreedomFI (a year off from work), leanFI, BaristaFI (part-time work), fatFI (you know that one), and even MOFI (“morbidly obese” FI). You’ll find your lifestyle comfort level– as long as you’re willing to work the months of life energy to afford it.

I’m a nuke and a hardcore spreadsheet nerd, so we didn’t seek much help from financial advisors. However, we spent many hours reading everything available in the 1980s and 1990s. When the Web exploded in the 21st century, we finally found our communities and crowdsourced even more advice. Today’s tools and retirement calculators are more widely available and better than ever before.

If that last paragraph doesn’t work for you, then it’s worth consulting a fee-only financial advisor. You can start with USAA’s free retirement review, or I’m happy to answer questions and help you find whatever type of advisor you want. (Interestingly, USAA recommends hanging on to your TSP account for as long as you can.) Take the advice you want, and then manage your own assets as simply as possible.

Most significantly of all, you’ll stay invested in an asset allocation which will at least keep up with inflation. This means that your own retirement spending smile will gradually drop your initial 4% SWR to an even more sustainable rate. Once you get there, you’re practically bullet-proof for life.

Your call to action:

- Take a look at the related links down there,

- Visit that USAA Life Uninterrupted link or give them a call, and

- Start planning your retirement lifestyle.

[earnist ref=”the-military-guide-to-financial-independence” id=”70177″]

Related articles:

Good News! How Our Nords Family Financial Independence Life Will Change In 2019

How Do You Survive A Stock Market Crash?

How (And Why) To Transfer Your TSP To An IRA (when the income-tax bracket is right)

Revealed: Our Asset Allocation During Financial Independence (new post on this coming soon)

Surprising Secrets Of Slow Travel

How Many Years Does It Take To Become Financially Independent?

Retirement: Relax, Reconnect and Re-engage

The “Fog of Work”

So here’s the question that’s been nagging me for a while (asked from a place of curiosity, not judgement): Are you spending your military pension checks *and* withdrawing from your investments? I ask for the sake of clarification, and because I think other (potential) military retirees might be curious. Thanks!

No worries, One Sick Vet, we all get to judge our own value of our spending!

I wrote this post for analyzing financial independence without a military pension. The numbers, ratios, and graphs are our actual spending (from our years of Quicken and Personal Capital data) and include the principal & interest payments on our home’s mortgage.

The post also assumes that we only have our investment portfolio to support that spending– no home equity, no rental income, no pensions.

This was the scenario we faced in 1999 when my spreadsheet showed that we had the investments to support the 4% SWR, yet we did not have my pension.

Today’s reality is that we’re spending my pension checks *and* withdrawing from our investments. Life is good.

When I was crunching the spreadsheet numbers, I also noticed the interesting drop in our non-discretionary spending.

Thanks, Doug. As you know, we just made a big move (for my health), and started all over again – new (to us) house to make weather resistant and energy efficient. Hopefully by next year we’ll have completed the major renovations that will make our house secure and energy-efficient, and our bills (non-discretionary spending) will go down correspondingly.

Doug

Thanks so much for sharing your insightful knowledge regarding FI. Can I reach you in private to discuss a personal matter regarding FI?

You bet, Angela. You can e-mail questions anytime to NordsNords at Gmail.